The word “discount” suggests a single number a vendor knocks off a price. In B2B SaaS it is closer to a distribution, shaped by how much a buyer knows, how long they commit, how much they consume, and when they sign.

Preparation is the main variable in that distribution: the buyers who prepare capture most of what is on the table, and a large share of everyone else gets nothing at all. The list price is mostly a number a vendor prints so it has something to mark down.

We meet these numbers in the wild: running competitors’ evaluations as a real prospect, asking for the discount like any buyer with a competing quote would, and recording where each vendor bends and where it holds.

We collected the most relevant, independently verified SaaS discount statistics we could source on how deep discounts go, how term length and volume change them, and what discounting quietly costs the vendor giving it. Every figure below is footnoted to its original source.

If you only keep a handful of these SaaS discount benchmarks, keep these:

The Average Is Falling While the Ceiling Holds

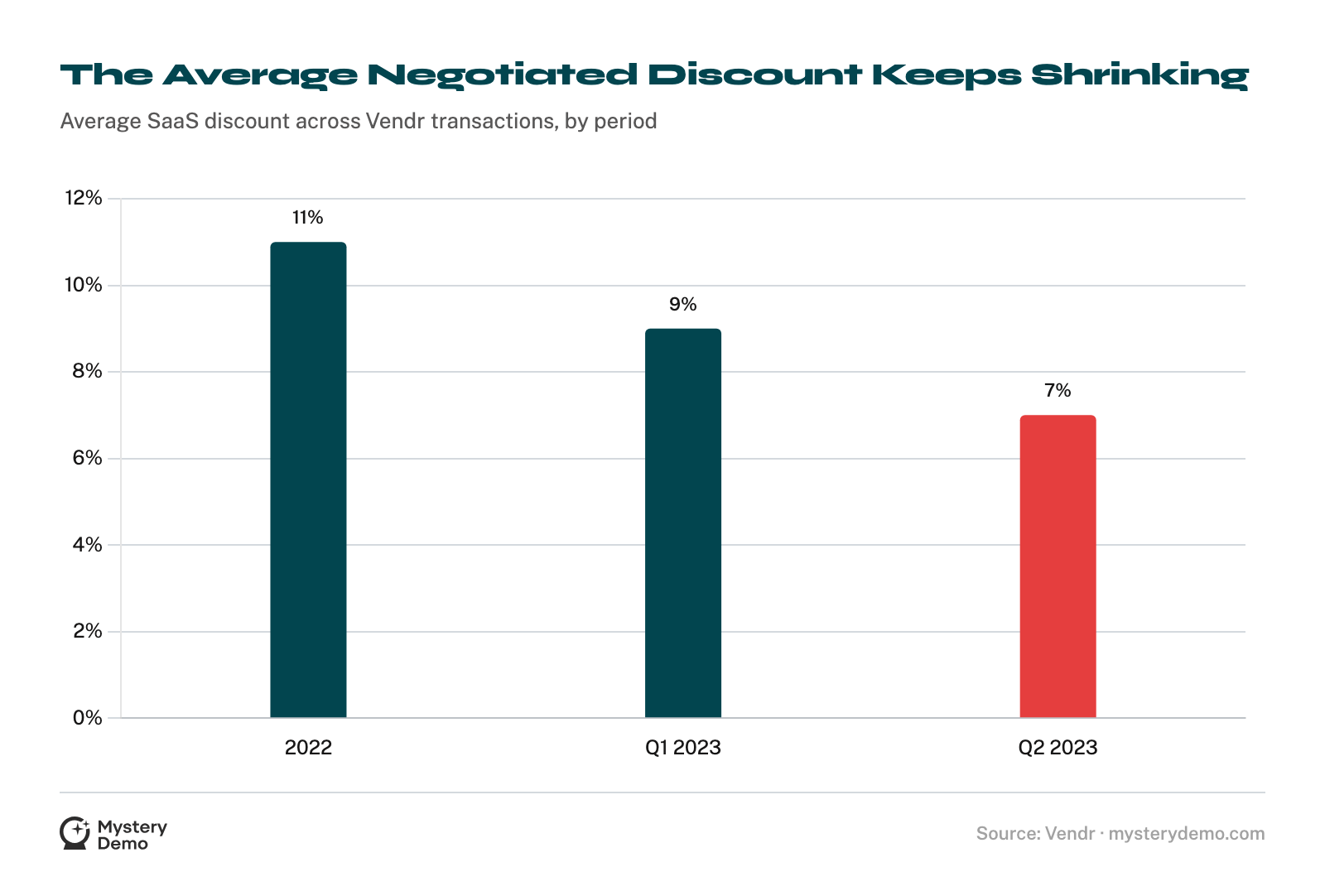

Vendor-side transaction data reads 11%, then 9%, then 7% across three consecutive periods. The direction of travel is down, not up.

Lay these next to each other and the shape of SaaS discounting appears. The blended average sits in single digits and is falling, while a prepared buyer reaches 20% to 35% below list, wider still in consumption-priced categories.

The average is low because most buyers barely negotiate. The ceiling is high because the ones who do are rewarded for information, not loyalty. Two buyers can purchase the same product in the same quarter and pay prices that differ by a third.

The Average Discount Hides Who Pays Full Price

Any “average SaaS discount” figure carries a quiet passenger: the large group of buyers who got zero. Ignore them and every benchmark reads too generously.

Two facts sit in tension here, and both are true. Almost every vendor discounts, yet a typical single-year buyer captures almost nothing. The bridge is that discounting is mostly ad hoc, handed out in the moment to whoever pushes.

That is the real cost of discounting for a vendor: margin that leaks one improvised concession at a time, to whoever happened to ask on the right call.

Multi-Year Is a Smaller Discount Than You Think

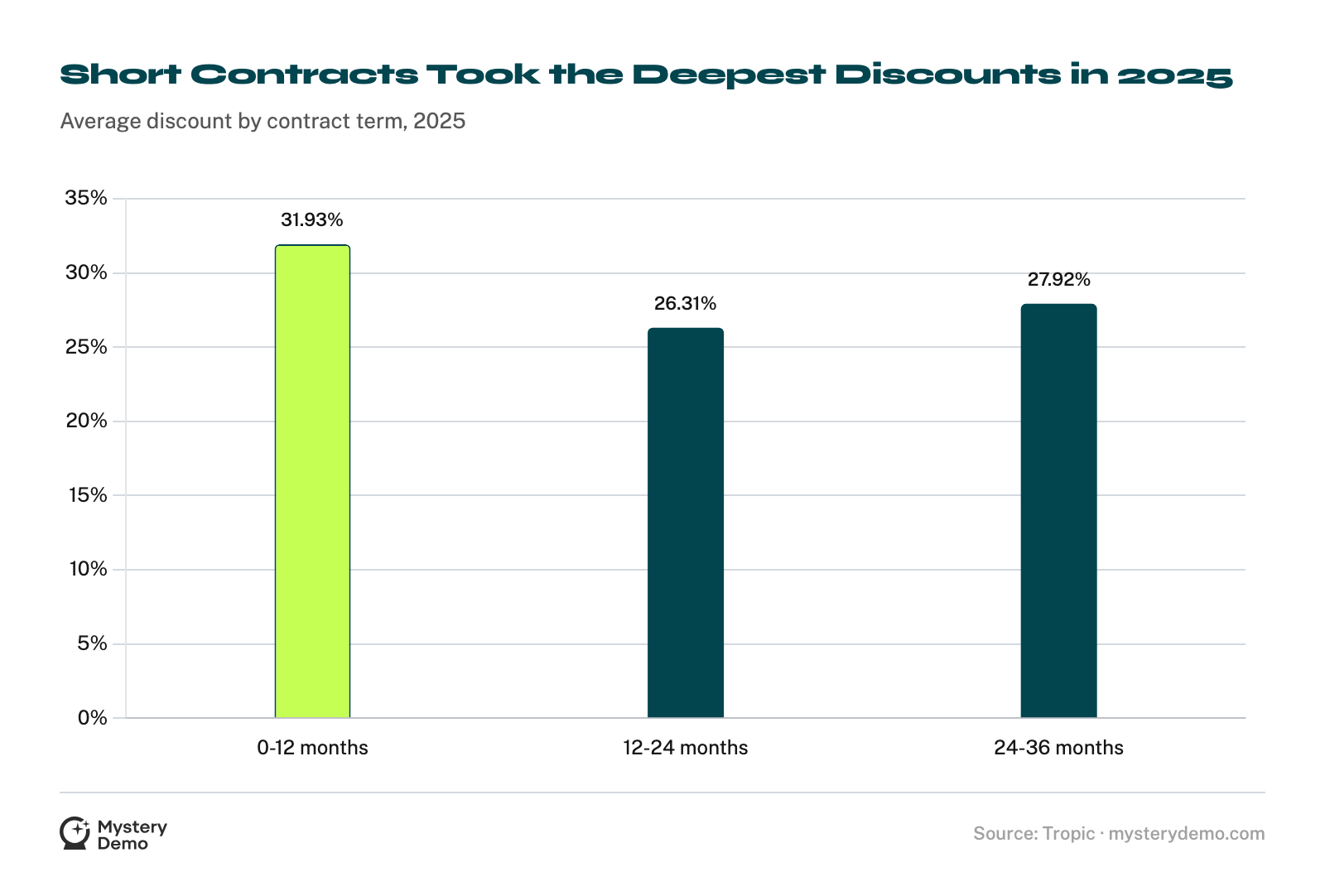

In 2025 the deepest average discounts came from the shortest contracts. The rest of the contract-level data explains why.

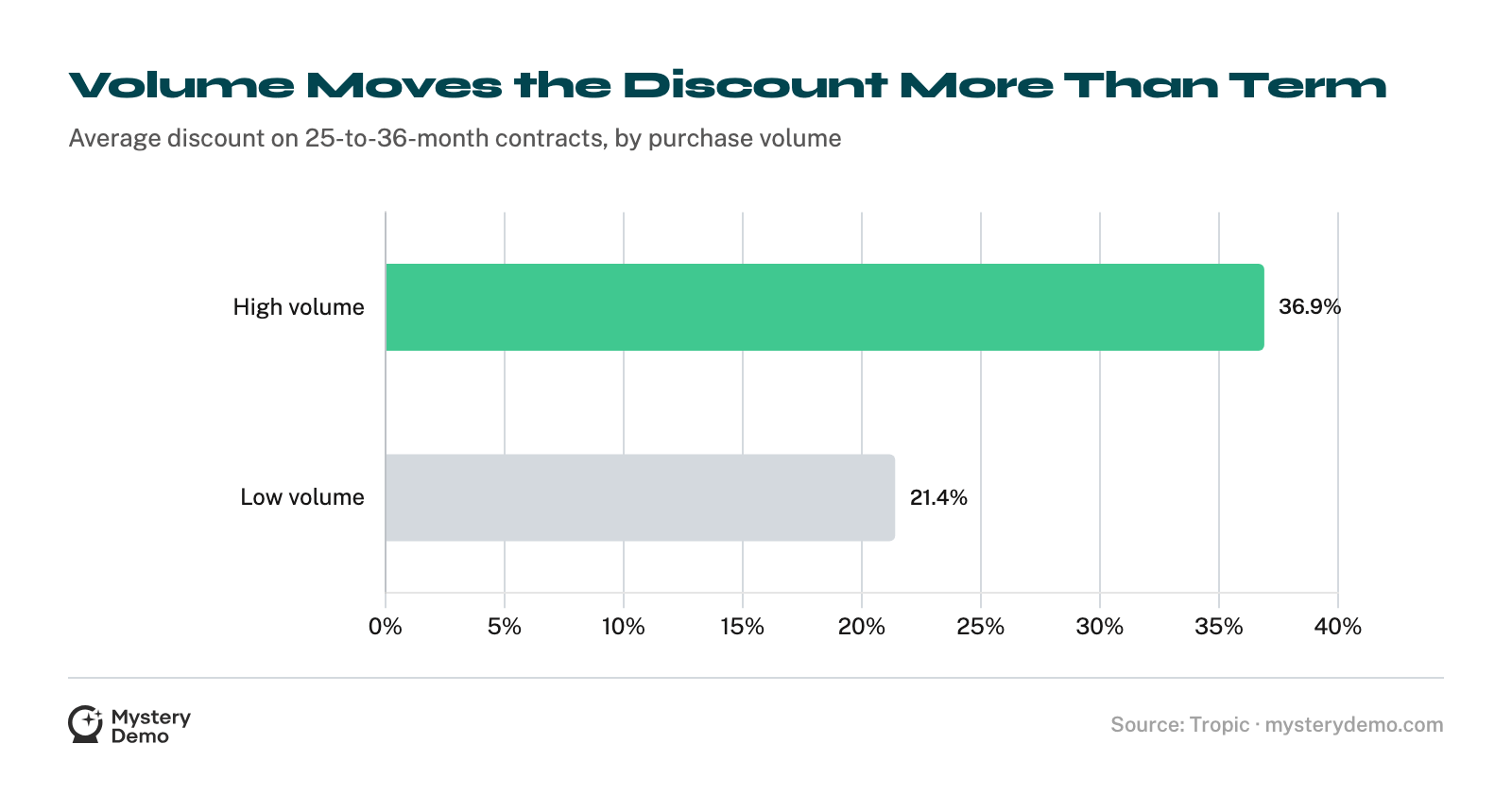

The multi-year signature most buyers count on is worth about 2 to 3 points. Volume is the lever that moves the number.

The deeper finding is the cost of staying put: vendors quietly trim the discount of the customer who keeps re-signing the same long deal, and reserve the best improvement for the buyer who held a single-year line.

Buyers seem to sense it, which is why many now trade the multi-year discount away for flexibility on purpose6.

For the structured teardown of a single rival, our SaaS competitor pricing research maps their discount behavior deal by deal.

.png)

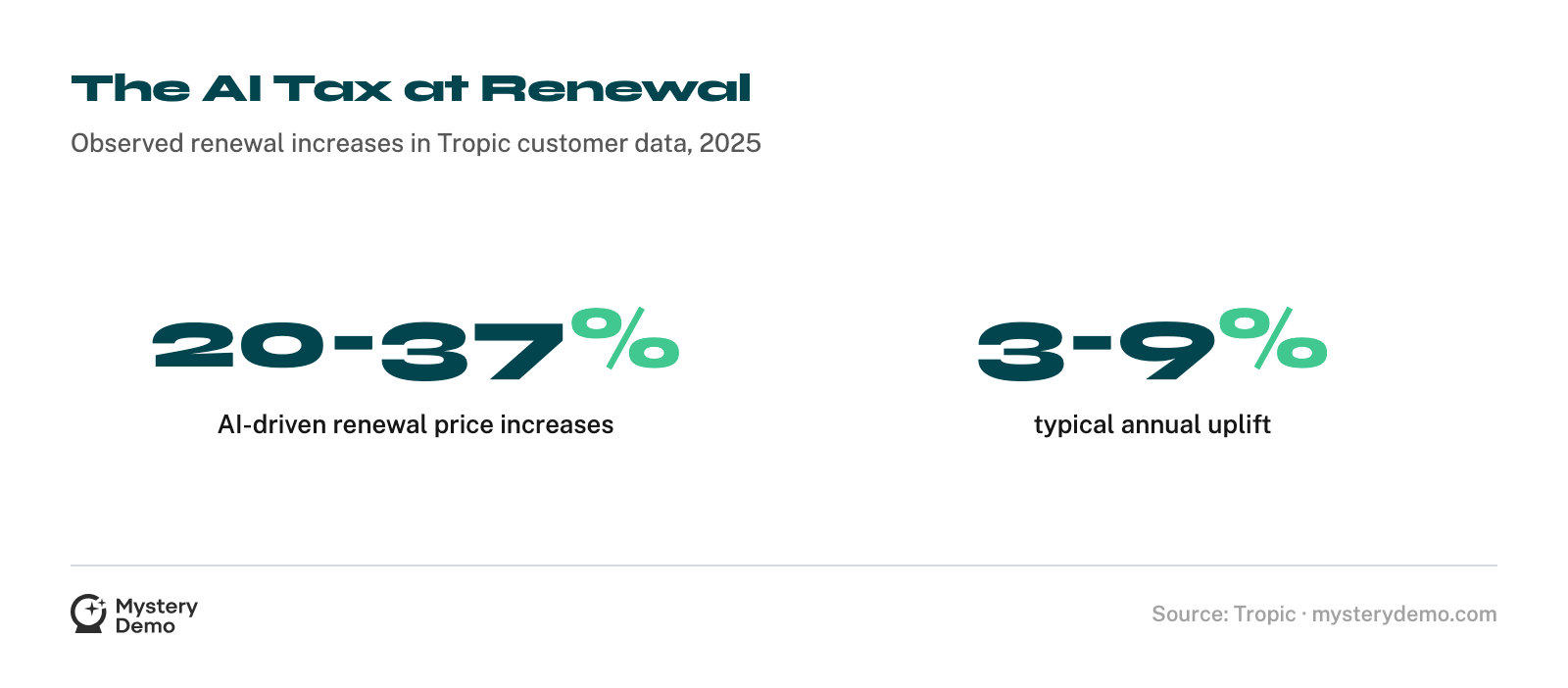

The AI Tax Turns Discounts Into Surcharges

The newest twist runs the discount conversation in reverse. In some categories the live question is how much the vendor will add on.

The conditional discount is worth pausing on, because it inverts the premise. A discount is normally a concession the seller makes to win a deal. Here the only way to access the saving on the base product is to buy the more expensive thing next to it.

It is a discount you can only collect by spending more. For a competitor watcher this is the most revealing pricing move of the current cycle, because it shows which vendors have decided AI is a margin opportunity rather than a feature.

None of these numbers tell you what your three closest competitors quote, discount, or surcharge once a buyer is in the room. Those numbers get spoken on live calls and never written down anywhere public.

So what does yours take when a buyer pushes twice and threatens to walk? Let’s go find their floor, and you can price your next deal against the real number instead of the published one.

Frequently Asked Questions

What is the average SaaS discount?

Single digits on a blended basis. The average negotiated discount fell to 7% in Q2 2023, down from 9% in Q1 2023 and 11% in 20221.

Are SaaS discounts getting bigger or smaller?

Smaller on average. Vendor transaction data shows the average discount declining from 11% to 7% across 2022 to mid-2023 as sellers push price discipline1.

How much can a well-prepared buyer save?

Far more than the average. The best-prepared buyers land 20% to 35% below list, and in consumption categories 20% to 40% better unit economics2.

Why is the average discount so low if some buyers save 30%?

Because the average is dragged down by buyers who get nothing. On initial deals, over half of single-year buyers land in the 0% to 10% bucket, and many pay full list price4.

Do most SaaS companies discount at all?

Almost all of them. Fewer than 5% of companies operate a no-discounting policy, so discounting is close to universal in B2B SaaS5.

Is SaaS discounting strategic or ad hoc?

Mostly ad hoc. In a 237-respondent poll, ad hoc discounting was by far the most common form, ahead of strategic and process-driven approaches5.

Does signing a multi-year SaaS contract get a bigger discount?

Less than buyers expect. Multi-year instead of single-year is worth roughly 2 to 3 percentage points of extra discount, not the double-digit jump many assume4.

Do longer SaaS contracts always carry deeper discounts?

No. In 2025 the deepest average discounts by term came from short-term (0 to 12 month) contracts at 31.93%, reversing 2024 when the longest deals led at 35.32%3.

What matters more for discount depth, term length or volume?

Volume. High-volume buyers on 25-to-36-month deals reached 36.9%, while low-volume buyers on the same term got only 21.4%3.

Does staying loyal on multi-year deals improve the discount?

The opposite. Buyers who start and stay multi-year see their discount erode by 1.3 points, while starting single-year and upgrading at renewal earns the best improvement at plus 2.5 points4.

How common are multi-year SaaS contracts?

Roughly a quarter to a third of deals. Multi-year incidence rose from about 25% of contracts in 2022 to about 30% in 20254.

Why do some buyers choose short-term contracts despite the discount?

To keep flexibility and limit risk. Buyers consciously trade away multi-year discounts for the freedom to walk, which is part of why the multi-year premium stays small6.

What is the AI tax in SaaS pricing?

A renewal surcharge tied to AI features. AI-driven price increases are running 20% to 37%, far above the typical 3% to 9% uplift3.

What is a conditional discount?

A discount on the base product offered only if the buyer adds AI SKUs, which reframes a higher total bill as a saving3.

How is a SaaS discount measured?

As the gap between the opening and closing price in a negotiation, tracked across more than 3,000 transactions and $240 million in spend in one quarter of vendor data1.

Does competition increase the discount you can get?

Materially. One documented buyer won a 30% discount on a new purchase by running a competitive evaluation and naming budget limits1.

What does discounting cost the vendor?

Mostly quiet margin loss. Because discounting is near-universal and largely ad hoc, the cost shows up less in the occasional deep deal than in routine concessions handed out without a policy5.

What is a realistic middle-ground SaaS saving?

Around the high teens. Vendr’s AI negotiation agent, trained on 130,000-plus outcomes, delivers an average of 17.1% savings, between the blended average and the best-prepared band2.

How do you find out what a competitor really discounts?

By watching their live deal, not their pricing page. Discount floors surface only under real buyer pressure, which is what we capture for you.

References

- Vendr: The SaaS Trends Report, Q2 2023 (2023)

- Vendr: The Pricing Intelligence Report 2025 (2025)

- Tropic: 2026 Software and AI Pricing Trends (2025)

- Mostly Metrics with Tropic: Your Guide to Negotiating Multi-Year Deals (2025)

- Ibbaka: SaaS Discounting Practices and Pricing (2023)

- Tropic: The 2023 SaaS Benchmarks Report (2023)

.png)