The B2B SaaS buyer you picture, one person with one budget and one yes to give, mostly does not exist. In their place is a committee: a shifting group of stakeholders who each get a vote, a veto, or at least a strong opinion they will share at the least convenient moment.

On your behalf, we go through a competitor’s sales funnel as a real buyer and multi-thread it the way a committee does, so we see every role they put in the room.

It is never one person. It is an SDR, then an account executive, then a sales engineer, and by the second call a procurement lead and a VP nobody had mentioned.

We collected the most useful, independently verified B2B SaaS decision maker statistics we could source on how that committee is built, who sits on it, and how long it takes to make up its many minds.

The short version: the group is large, cross-functional, and has largely decided before a single rep is in the room. Each stat below is footnoted to the research it came from.

If you only keep a handful of these, keep these:

The Buying Committee Is Always Bigger Than One

Ask three research firms how many people are on a B2B buying committee and you get three different numbers, because they are counting three different things. The honest answer is a group, and how big depends on who you count.

That spread is not noise. Gartner is counting decision-makers inside the buying organization, Forrester is counting the wider network of internal stakeholders and outside advisors, and the gap between them is the part most vendors never see: the colleagues, consultants, and peers shaping the call from offstage.

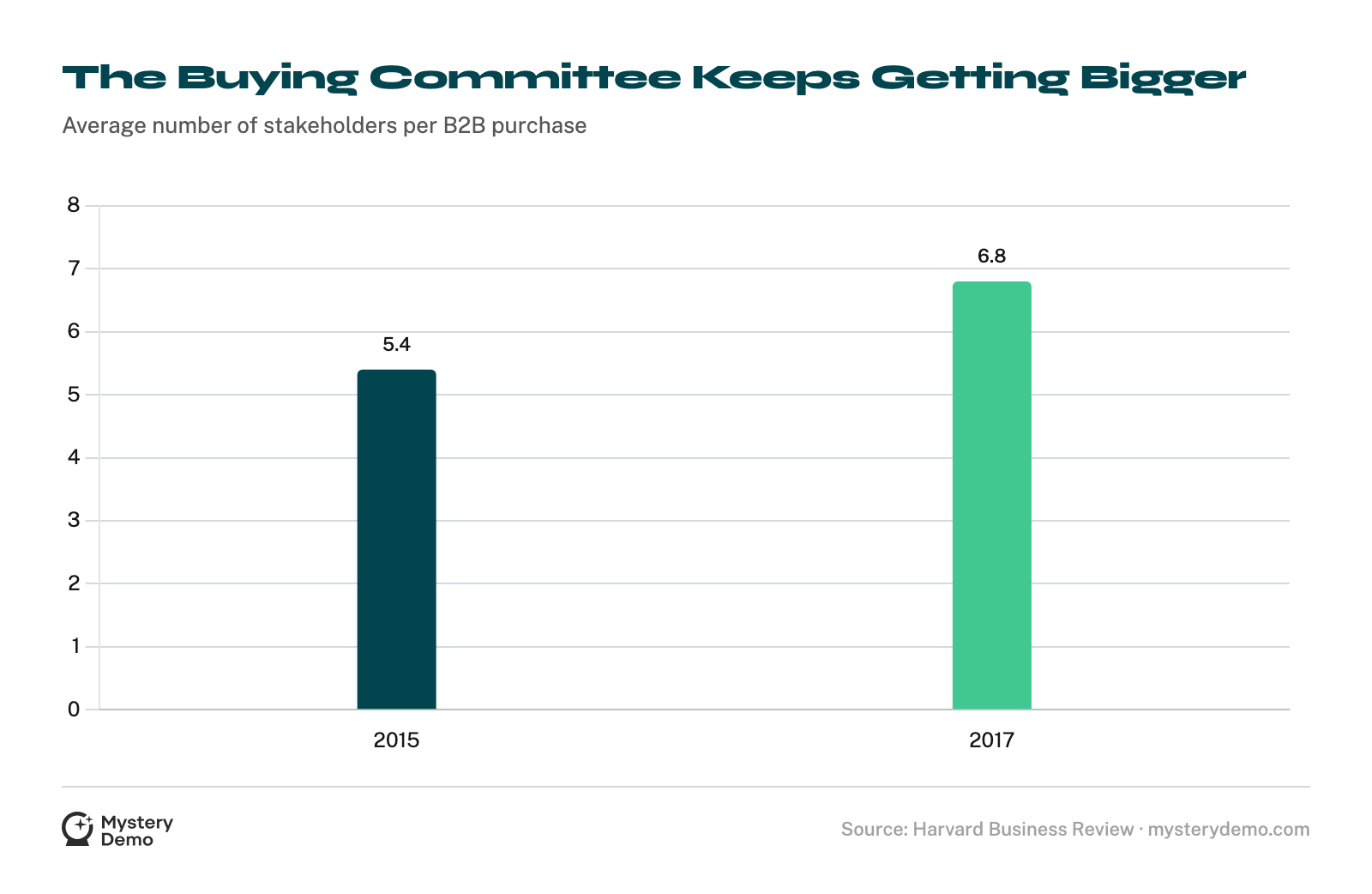

The committee has grown over the past decade, too. The average climbed from 5.4 to 6.8 people between roughly 2015 and 2017, and it has only widened since10.

Not every source says committees are growing, though. Some show them consolidating into smaller, more senior groups.

Both readings are true, and two forces explain them. Group size scales with deal size: a 3-person group buys a $20,000 tool, a 16-person group buys a platform.

On top of that, the overall mix is tilting toward smaller, faster purchases, which is what G2’s year-over-year shrink is picking up.

For anyone studying a competitor, the headline average matters less than the shape of the group around a deal like yours, and that shape only shows up when you watch the whole evaluation, not a single call.

Every Seat on the Committee Wants Something Different

Size is only half the picture. What makes the committee hard to read is that it is cross-functional by design, and the mix tells you who you are really selling to. The person running the demo is rarely the person signing the contract.

Two of those numbers sit in tension. A single owner exists, a C-suite exec or the CFO, in 42% of deals, yet 82% of buyers still call the choice consensus-based.

Both are true: someone is ultimately accountable, and that person’s yes is hostage to a consensus they do not fully control.

It is also why a competitor’s demo is a poor sample of their real sales motion.

The sales engineer is selling to the end user and the champion in the room, but the real decision comes later, with the VP, the CFO, and a procurement lead who were never on the call you sat through.

.png)

A formal committee is also the default now, not the exception. 68% of organizations run a buying committee, including the 19% that formed one for the first time in a single recent year15. The buying group is the unit of decision, and the practice is still spreading.

They’ve Mostly Decided Before You Hear From Them

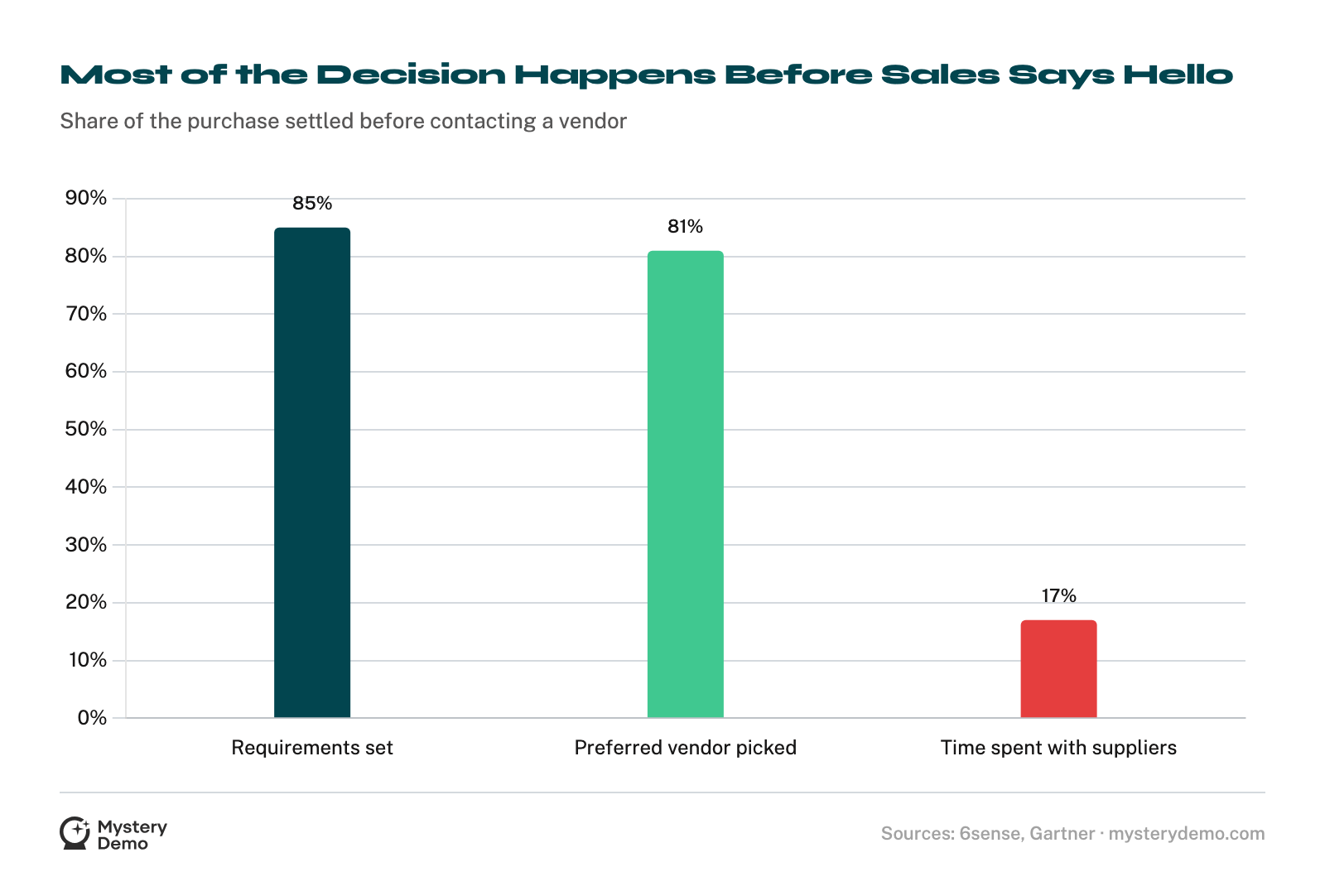

The committee does the bulk of its work before any vendor knows it exists. By the time a rep gets a hello, the shortlist is built and ranked.

This is the demand-generation reality behind the committee: most of your future buyers are not even looking yet. Up to 95% of business buyers are out of the market for a given product at any one time18. When the 5% do start, they begin with the vendors they already know.

Even with 81% walking in with a favorite, the demo still matters, because two contests run in sequence.

Familiarity wins the first, deciding who even makes the shortlist, which is why the 95% who are out of market and the 97% who already know a vendor weigh so heavily. The live evaluation wins the second, deciding who closes among the shortlisted.

For anyone studying a competitor, only the second contest is observable. The research stays private; the sales process does not, and it can be walked thread by thread, exactly the way a real committee walks it.

Consensus Is Where Deals Go to Stall

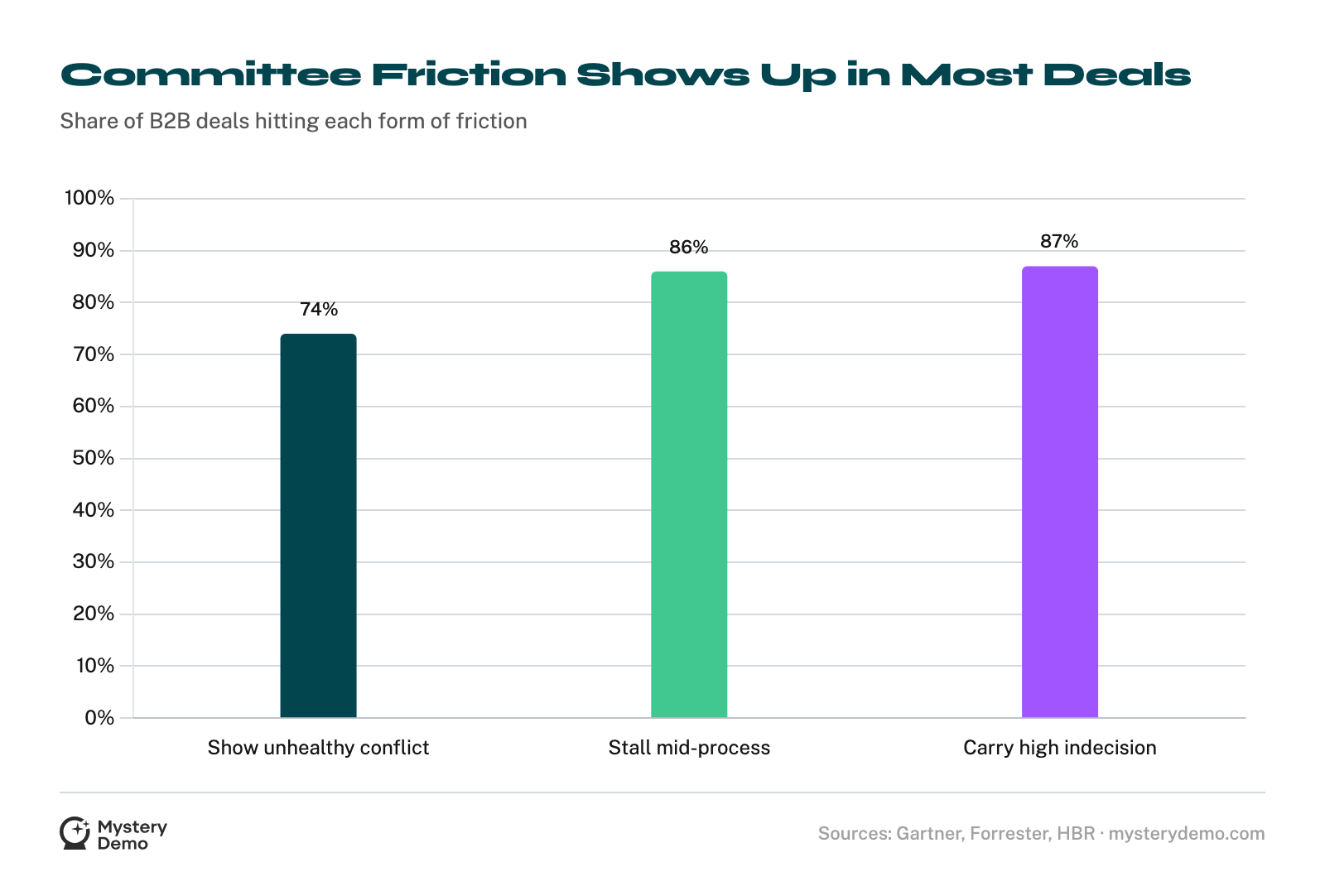

A confirmed favorite still has to clear the committee, and clearing it is where the calendar gets away from everyone. A bigger committee buys more carefully and far more slowly, because more stakeholders means more agendas to reconcile, and a committee is very good at saying no by saying nothing.

The average cycle is compressing as smaller, simpler deals close faster, while the hard, high-consideration purchases stretch out, so the mean falls even as the painful tail gets worse.

On the slow deals the mechanism is information overload, not laziness. When a committee drowns in contradictory inputs, buyers are 153% more likely to settle for a smaller, more cautious purchase than they first planned20.

The cost of the committee shows up twice: once as a longer calendar, and again as a shrunk deal.

A typical complex purchase takes twice as long as buyers expect, and 65% say they burned as much time getting ready to talk to a rep as they had budgeted for the entire purchase10.

For competitive research, the stall rate is the opening. If 86% of a category’s deals lose momentum somewhere in the committee, fixing that one friction point pulls deals away from the rivals who never noticed where they stalled.

You just have to know where the friction lives, which means watching the full sales process, not the highlight reel.

The Committee Wants to Buy Without You

Self-service is the default now, and the committee spreads its research across a widening set of channels before anyone dials a rep.

It helps that buyers rarely start cold: 78% have already heard of the product they end up buying, so self-navigation feels safe. Whether that preference serves them is messier than it looks.

Buyers who drive the process themselves do better than the ones a rep drives: 65% of self-navigated purchases were high-quality, against just 24% of rep-led ones16.

But going fully alone is not the answer either. Buyers are 1.8x more likely to close a high-quality deal when they pair a vendor’s tools with a rep than when they go without one8, and pure self-service tracks with more purchase regret.

The mode that works keeps the committee in control, backed by the vendor’s tools and a rep who shows up at the right moment.

The practical read is that the human sale still decides the deal. It just happens later, in front of more people, and only after the committee has tried to do without it.

The edge goes to competitors whose self-serve tooling and late human sale are stitched together.

Whether you are defending a category or sizing up one you want to enter, what you are really studying is how each rival handles that late, crowded handoff, because that is where a committee’s pre-formed favorite gets confirmed or overturned.

Their internal buying meetings are closed to you. Their sales process is not, and you can move through it exactly the way their buyers do.

We run your competitors’ full buying process the way a committee would, then hand you the whole playbook: who they put in the room, what they show the technical buyer versus the economic one, where they discount, and where the deal leaks.

Let’s map their committee together, and you will see which story they tell each seat, plus the one place those stories stop matching.

Frequently Asked Questions

How many people are on a B2B SaaS buying committee?

It depends who you count, but the group is always larger than one. Gartner puts buying groups at 5 to 16 people across up to four functions1, 6sense reports an average of 11 people2, and Forrester counts 13 internal stakeholders plus 9 external influencers3.

What is the average size of a B2B buying group?

The most commonly cited average is 11 people, per 6sense’s 2024 research2. Forrester reports an average of 13 people involved within the organization9.

Has the B2B buying committee grown over time?

Yes. The average number of stakeholders rose from 5.4 to 6.8 between roughly 2015 and 201710 and has widened since, though some 2025 data shows the largest committees consolidating into smaller, more senior groups11.

Are buying committees getting bigger or smaller?

Both, depending on deal size. Forrester sees groups growing3, while G2 reports the once-dominant 5-to-8-member committee shrinking 11 points year over year as 3-to-4-person groups rise11. Larger, more complex purchases pull in more people; smaller deals are consolidating.

How many departments are involved in a B2B purchase?

89% of B2B purchases involve two or more departments9, and Gartner finds buying groups spanning as many as four functions1.

Who is on a typical SaaS buying committee?

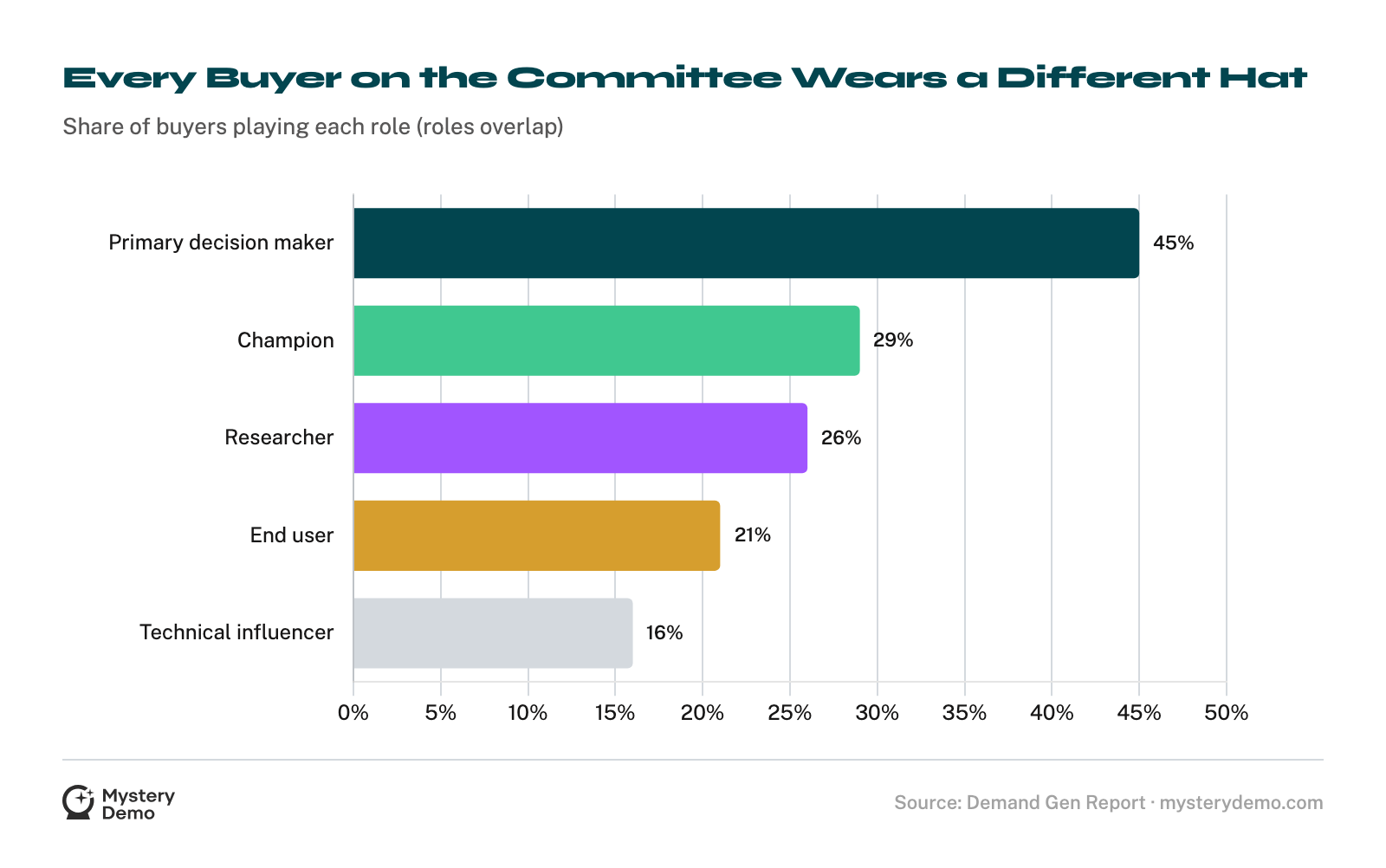

A mix of roles: primary decision makers (45%), champions (29%), researchers (26%), end users (21%), and technical influencers from IT, Legal, or Operations (16%)15. Procurement are decision-makers in 53% of cycles3 and IT is involved in nearly half of software decisions11.

Who has final say in a B2B software purchase?

42% of buyers name a C-suite executive or the CFO as ultimately responsible, but 82% describe the decision as consensus-based rather than one person’s call14.

How senior are B2B software decision-makers?

More senior than ever. 52% of tech decision-makers hold VP-level titles or above12.

How much of the buying journey happens before contacting sales?

Most of it. Buyers reach first contact only 61% of the way through their journey7, and 85% establish their requirements before ever contacting a vendor4.

Do buyers already have a preferred vendor before talking to sales?

Usually. 81% of buyers have picked a preferred vendor before they talk to a rep4, and the winning vendor sits on the Day One shortlist 85% to 95% of the time7.

How much time do buyers spend with sales reps?

Very little. Buyers spend just 17% of total purchase time meeting with potential suppliers, and that is split across every vendor they consider5.

What is the 95-5 rule in B2B?

It is the finding that up to 95% of business buyers are not in the market for a given product at any one time, leaving only about 5% actively buying18. It explains why brand familiarity shapes shortlists long before a demo.

How long is the average B2B SaaS sales cycle?

About 10.1 months in 2025, down from 11.3 months the prior year7. For purchases over $20,000, 49% of buyers took four months or more just to decide14.

Why do bigger committees take longer to decide?

More stakeholders means more agendas to reconcile. 74% of buyer teams show unhealthy conflict during the decision1, and 86% of purchases stall mid-process9.

How often do B2B deals end in no decision?

Between 40% and 60% of deals are lost to no decision, with 87% of opportunities carrying moderate-to-high customer indecision6.

Does committee size affect deal size?

It can shrink it. When a committee faces too much contradictory information, buyers are 153% more likely to settle for a smaller, more cautious purchase than they originally planned20.

Do B2B buyers prefer to buy without a salesperson?

They say so. 75% of buyers prefer a rep-free experience8, and nearly two-thirds prefer to engage sales only in the late stages, up 17 points in a year11.

Do rep-free purchases go better?

No, and that is the paradox. Only 24% of rep-led purchases were high-quality versus 65% of self-navigated ones16, yet buyers are 1.8x more likely to close a high-quality deal when they pair vendor tools with a rep rather than going alone8.

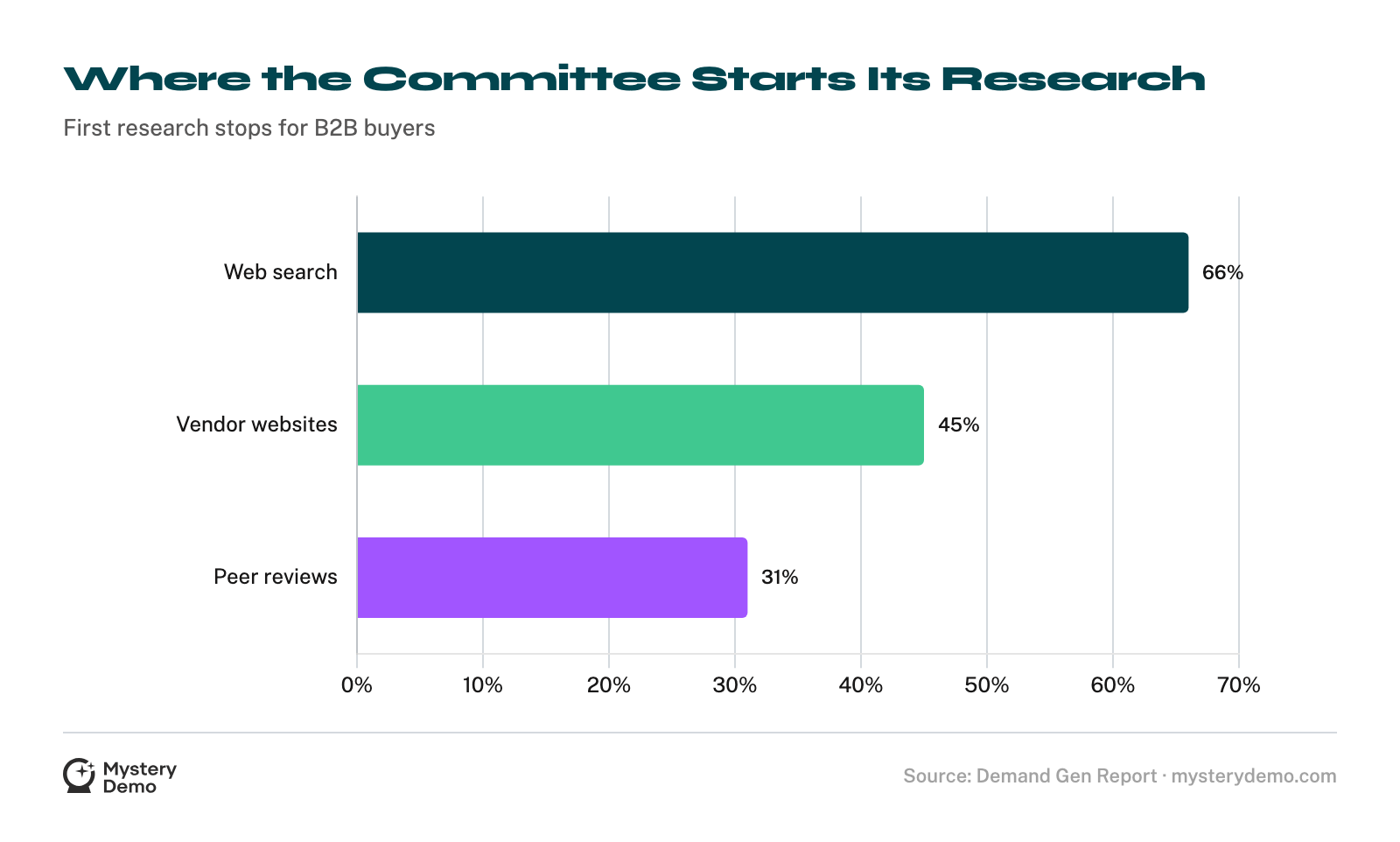

How many channels do B2B buyers use?

Ten or more, double the five they used in 201617. Their first stops are web search (66%), vendor websites (45%), and peer reviews (31%)19.

How much do peer reviews matter to buying committees?

Enough to shape the shortlist. Peer reviews are among buyers’ first research stops, consulted by 31% of buyers19, and 78% had already heard of the product they bought before research even began12.

What does the buying committee mean for competitive research?

It means a single demo shows you a fraction of how a competitor really sells. The deal is decided by stakeholders you never meet, across channels you cannot see, so understanding a rival’s sales motion requires capturing every stakeholder thread, which is exactly the multi-threaded work we do.

How do you research how a competitor sells to a buying committee?

You go through their funnel the way a real committee does: book the demo, multi-thread across the SDR, account executive, and sales engineer, and document who they put in the room and where they discount. That is exactly the work we deliver.

References

- Gartner: Sales Survey Finds 74% of B2B Buyer Teams Demonstrate Unhealthy Conflict During the Decision Process (2025)

- 6sense: 2024 Buyer Experience Report (2024)

- Forrester: The State of Business Buying, 2026 (2026)

- 6sense: The 2024 B2B Buyer Experience Report (2024)

- Gartner: 80% of B2B Sales Interactions Will Occur in Digital Channels by 2025 (2020)

- Harvard Business Review: Stop Losing Sales to Customer Indecision (2022)

- 6sense: 2025 B2B Buyer Experience Report (2025)

- Gartner: The B2B Buying Journey (2023)

- Forrester: To Master B2B Buying Mayhem (The State of Business Buying, 2024)

- Harvard Business Review: The New Sales Imperative (2017)

- G2: 2025 Buyer Behavior Report (2025)

- TrustRadius: 2024 B2B Buying Disconnect Report (2024)

- Demand Gen Report: 2022 B2B Buyer Behavior Survey (2022)

- G2: 2024 Buyer Behavior Report (2024)

- Demand Gen Report: 2021 B2B Buyers Survey Report (2021)

- Gartner: 83% of B2B Buyers Prefer Ordering or Paying Through Digital Commerce (2022)

- McKinsey: B2B Sales, Omnichannel Everywhere, Every Time (2021)

- Ehrenberg-Bass Institute, John Dawes: The 95:5 Rule (2021)

- Demand Gen Report: 2024 B2B Buyer’s Survey (2024)

- Gartner: New B2B Sales Approach to Win in Today’s Information Age (2019)

.png)