Almost every company says it does competitive intelligence. Far fewer can tell you who the competitor put on the call, how the renewal quote read, or where the demo quietly fell apart.

That gap is the whole story of modern CI: the function is everywhere, the headcount is thin, and most of the work is reading the same public sources every rival is already reading.

Collecting that intelligence first-hand is the part almost no CI program has the people to reach. On your behalf, we become a buyer inside a competitor’s funnel, take the demo, get the real pricing, and open a renewal, then hand back the intelligence gathered from inside their own sales process.

We pulled together the most useful, independently verified competitive intelligence statistics on how common CI really is, how it is staffed, and where it falls short.

One honest note on sourcing: the freshest, glossiest CI numbers tend to come from the CI software vendors themselves, which is a little like asking a barber whether you need a haircut.

We stuck to independent academic and analyst research, even where a figure runs a few years older than the marketing-deck version. Every number below is footnoted to its original source.

If you only keep a handful of these, keep these:

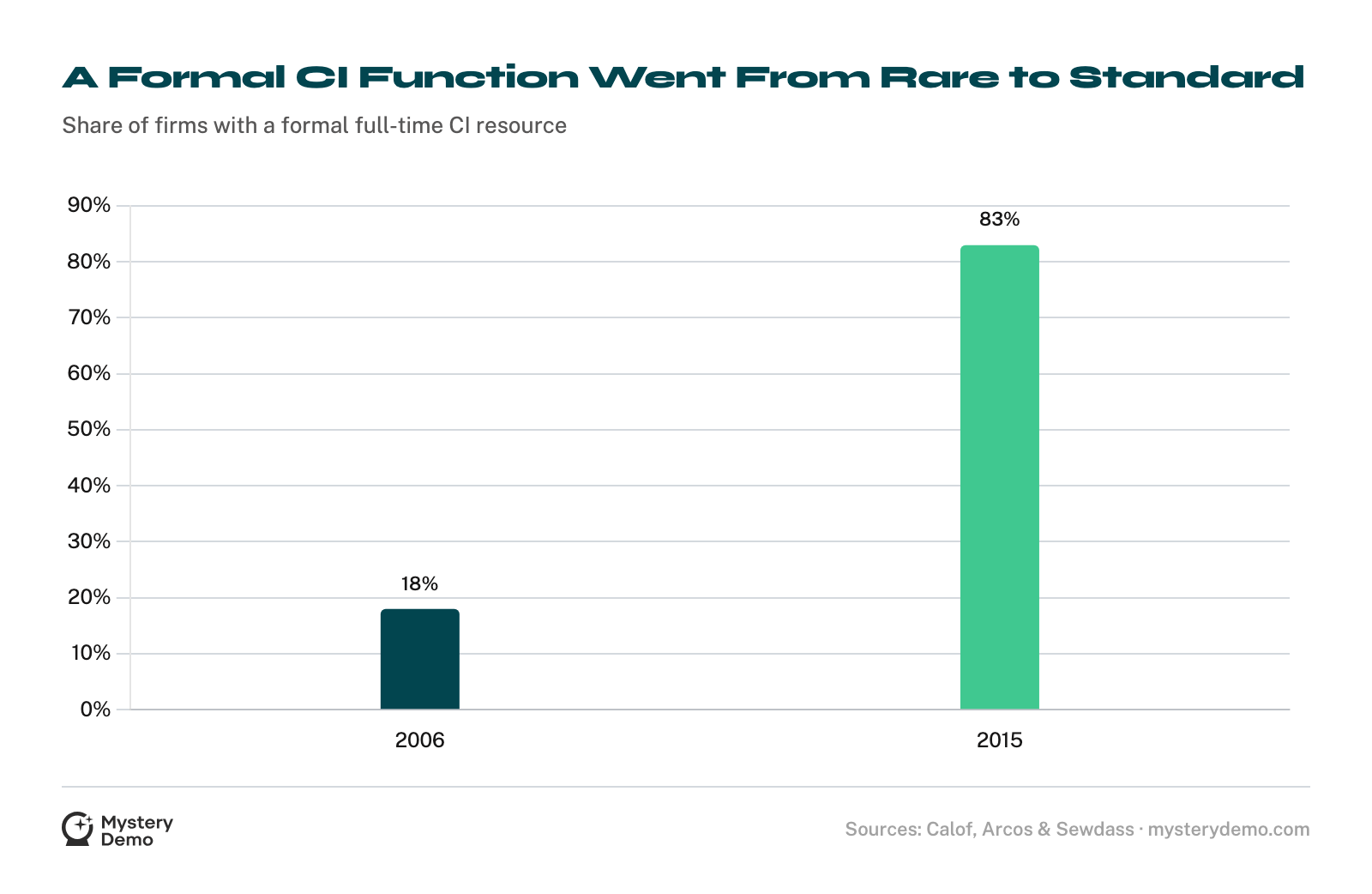

Almost Every Serious Company Now Runs CI

Competitive intelligence used to be a rare, elite capability. It is close to standard equipment now, and it got that way fast.

The 18%-to-83% jump is the headline trend: in under a decade, a formal CI resource went from a minority habit to the default.

The reason competitive intelligence feels less like a moat than it used to is hiding in plain sight. If 87% of your competitors have a CI function too, then having one is table stakes rather than an edge.

The edge has moved to what the function really does, and that is where the numbers get less flattering.

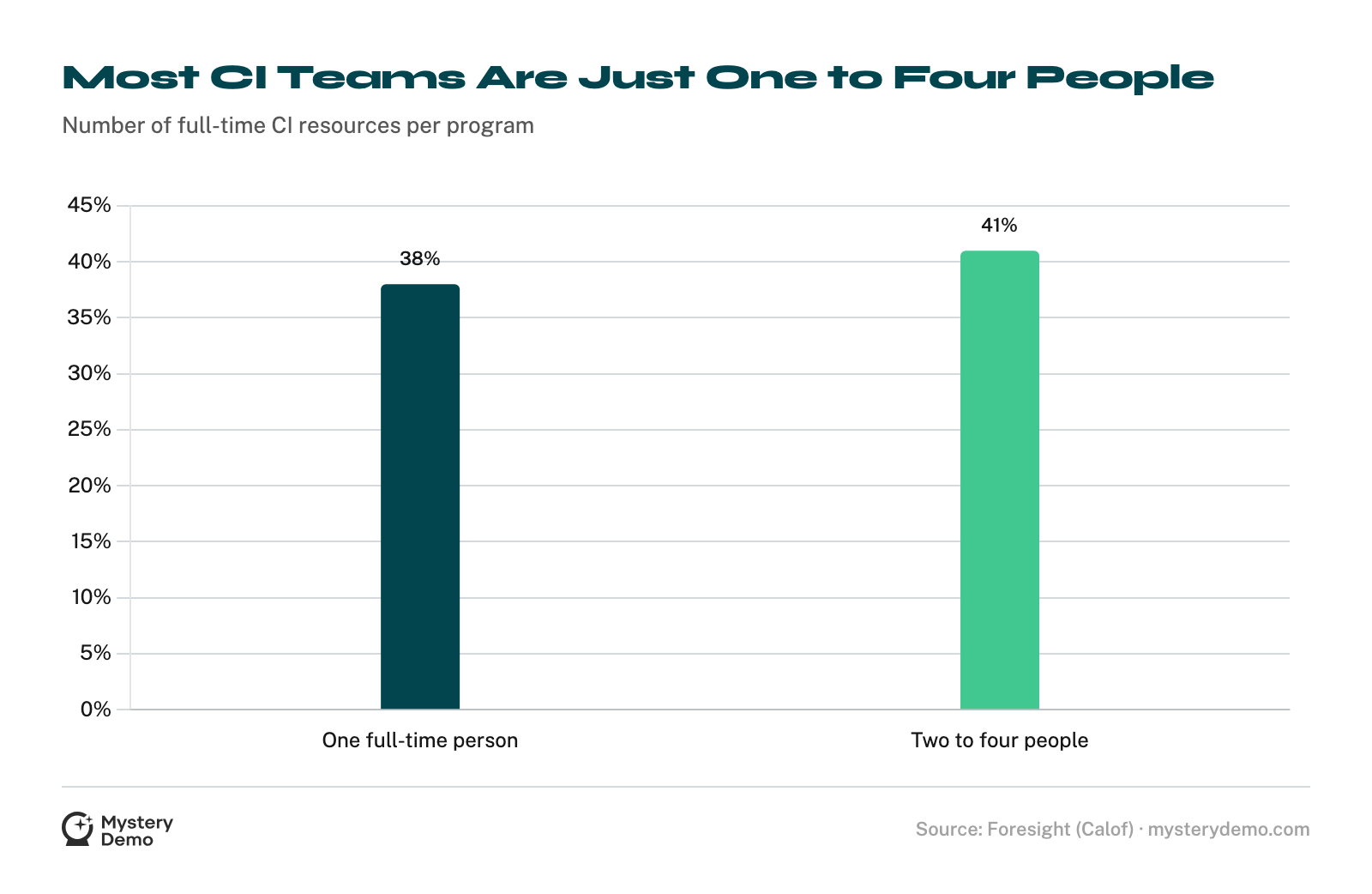

But the CI Team Is Usually Tiny

For a function this widespread, competitive intelligence is staffed like an afterthought. The typical CI “team” is one or two people wearing several other hats.

Put the size and the placement together and you get the real constraint. A one-person CI function buried inside the marketing team keeps a battlecard roughly current. Shopping a competitor end to end, sitting through their demo, and pressure-testing their renewal takes hours that function was never staffed for.

The constraint here is arithmetic. When the whole function is half a person’s week, the work that survives is whatever can be done from a desk, and that quietly decides what counts as intelligence in most companies.

Most CI Is Desk Research, Not Field Work

The dominant form of competitive intelligence is reading, and most of what gets read is the same public material every rival already has.

This pattern should bother most heads of product marketing. If the most-used inputs are newspapers, the open web, and your own colleagues, then your competitive intelligence is built almost entirely from sources your competitor controls or your team already believes.

Nobody in that mix has been inside the rival’s funnel as a real buyer. The result is intelligence that is accurate about the public story and blind to the private one: the actual pitch, the actual objection-handling, the actual price after negotiation.

Desk research tells you what a competitor says. It cannot tell you what they do when a prospect is on the line.

.png)

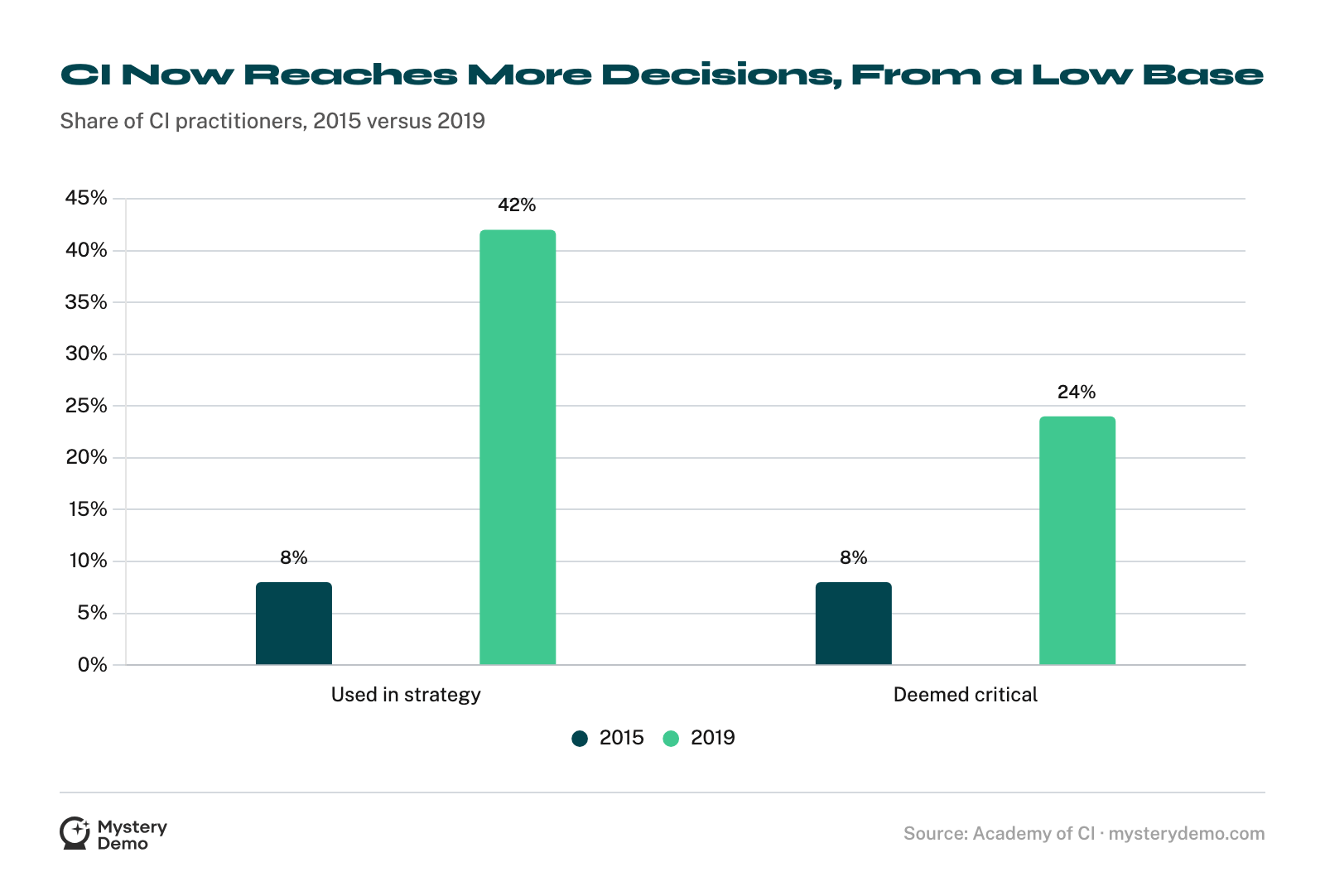

The Programs That Get Out From Behind the Desk Win

The payoff for doing the harder kind of research is not theoretical. The firms that research more, and research first-hand, measurably pull ahead.

The two halves of this fit together. High-growth firms research more often and lean on primary research, and they get more out of it. Meanwhile, across the field, most CI still does not reach the decision, with under half of practitioners seeing their work used strategically and only a quarter calling it critical.

The gap between those two facts is the opportunity. Intelligence that changes a decision tends to be the kind nobody else has, gathered by watching how a competitor really sells rather than reading the press release everyone already has.

The programs climbing toward that 24% are the ones that stopped settling for second-hand.

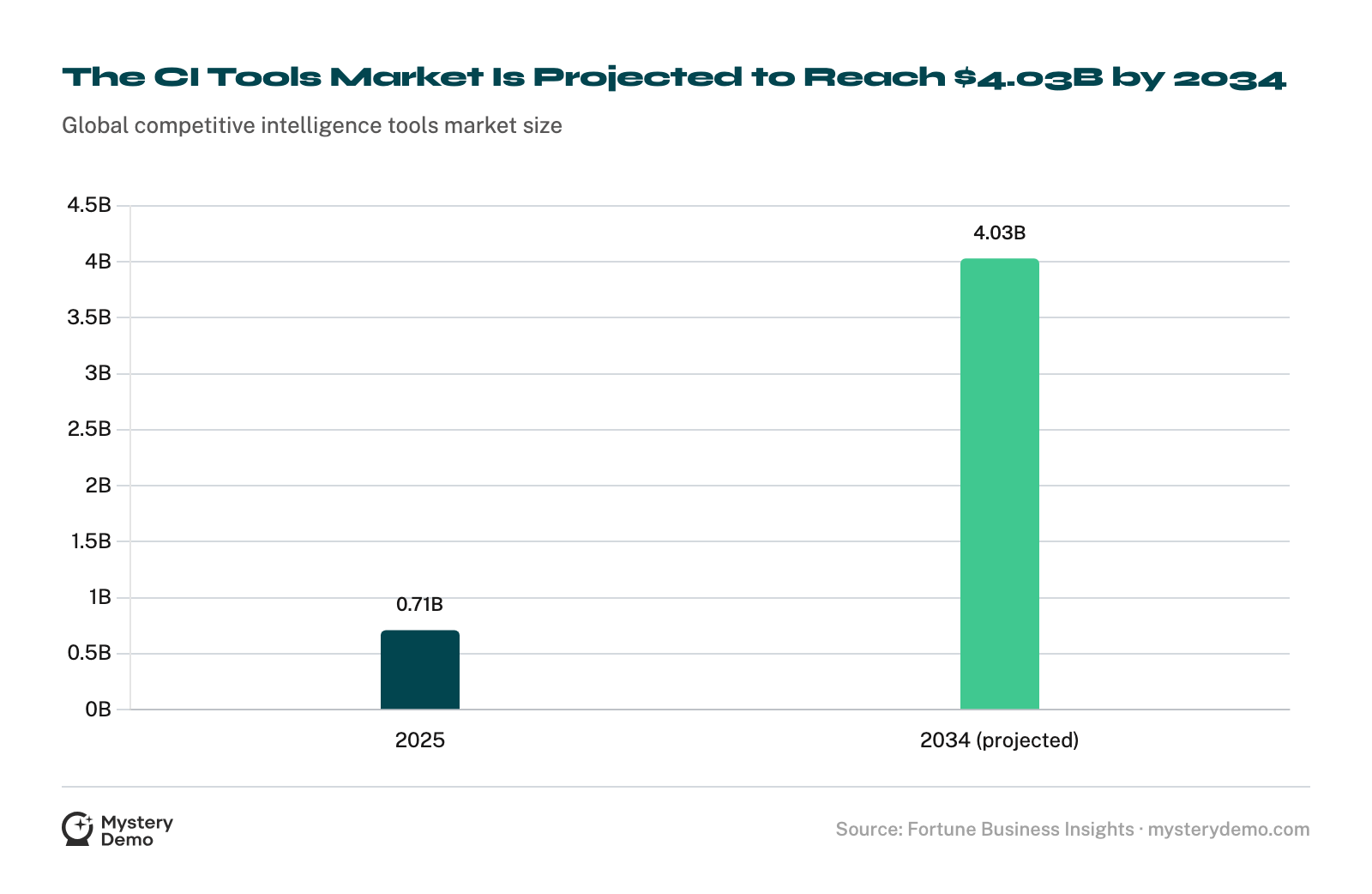

CI Spending Is Climbing

Companies are pouring more money into competitive intelligence, even as the work itself spreads beyond any single team.

The spend and the spread point the same direction: competitive intelligence is being taken more seriously and pushed into more hands at once. That is both good news and a quiet trap, because more tools and more people scale a sourcing problem instead of fixing it.

A bigger budget aimed at the same public inputs just buys more of what your competitors already publish about themselves.

The investment only turns into an edge when some of it buys the buyer-side view a desk cannot reach: the real demo, the real pricing, the renewal conversation.

If your CI program is strong on the public record and thin on the private one, the cause is the same one the whole industry shares: too little headcount and too few hours. We close that gap.

On your behalf, we run that same evaluation as a real buyer and renewing customer, then hand back what a desk cannot reach: how they pitch, where they dodge, what they charge, and when they discount. For the structured side-by-side, our competitor product comparison turns what we find into a decision-ready map.

Bring us your competitor list and your analysts can keep covering the public record while we go get the private one.

Frequently Asked Questions

What share of companies have a competitive intelligence function?

Nearly all serious B2B firms. In a survey of European firms, 87% had a formal CI structure1, and among practicing CI professionals, 84.8% had a CI manager and 61% a formal centralized unit2.

How fast did competitive intelligence become standard?

Quickly. The share of firms with a formal full-time CI resource rose from 18% in 2006 to 83% in 20151, which is why simply having a CI function is no longer a competitive edge on its own.

How big is a typical competitive intelligence team?

Small. 38% of practitioners have a single full-time CI resource and 41% have two to four2; almost half report one or fewer full-time-equivalent people on CI4, and where a formal unit exists, 83% employ fewer than 10 staff3.

Where does competitive intelligence sit in the org?

Usually inside another team. 79% of formal CI units sit within marketing, market research, or corporate planning3, and only about a third operate as a stand-alone unit, up from 10% in earlier research4.

Do most CI teams do primary or secondary research?

Overwhelmingly secondary. CI professionals spend the majority of their time on secondary data collection and rate secondary sources as more important than primary ones4, which means most competitive intelligence is desk research, not field work.

What are the most-used competitive intelligence sources?

Public ones. The two most frequently used CI sources are newspapers and periodicals, then the Internet, with external impersonal sources used significantly more than personal sources3. Even the primary research that happens leans on internal employees rather than the competitor4.

Does doing primary research pay off?

Measurably. Among professional-services firms, high-growth ones are 3x more likely to research their market frequently and see 30% more impact from primary research than slower-growing peers5.

How often does competitive intelligence influence strategy?

Less than you would hope. Only 42% of CI practitioners see their intelligence used in strategic decisions, and just 24% say their input is deemed critical, though both figures have roughly tripled or better since 20156.

How big is the competitive intelligence market?

One market-research firm estimates the competitive intelligence tools market at $0.71B in 2025, growing to $4.03B by 2034, a 21.17% CAGR7.

Is more competitive intelligence budget worth it?

Spending is climbing: the CI tools market is growing at a 21% CAGR7 and 30.7% of product-marketing teams increased investment in 20258. But more budget aimed at the same public sources scales the problem instead of solving it. The spend that pays off buys the intelligence a competitor never volunteers.

Is CI a dedicated job or a shared skill?

Increasingly shared. Dedicated CI producers fell from 58% of practitioners in 2015 to 30% in 2019, with the rest now both using and producing intelligence6, as CI spreads across product, marketing, and sales.

Why is so much competitive intelligence easy to replicate?

Because most of it is built from the same public inputs every rival uses: newspapers and the open web3. When everyone reads the same sources, the resulting intelligence converges, and no one gains an edge.

What is the biggest gap in most competitive intelligence programs?

First-hand observation of how a competitor really sells. With tiny teams4 spending most of their time on desk research4, almost no program has the hours to go through a rival’s funnel as a real buyer, which is the one source no amount of desk work can replace.

What counts as primary-source competitive intelligence?

Intelligence you collect directly rather than read second-hand: sitting through the competitor’s demo, getting their pricing, testing their objection-handling, starting a renewal. Going through a competitor’s funnel as a real buyer is exactly this kind of primary research, gathered from inside their own sales process.

How does first-hand buyer research fit into a CI program?

It supplies the field data your desk research cannot. Your analysts keep covering the public record; the first-hand work covers the private one, capturing what a competitor really sounds like in the room, from the opening pitch to the price after you push back, then feeds it into your battlecards and a competitor product comparison.

References

- Calof, Arcos and Sewdass: Competitive Intelligence Practices of European Firms, Technology Analysis and Strategic Management (2018)

- Jonathan Calof: Canadian Competitive Intelligence Practices, Foresight, Emerald Publishing (2017)

- Yap and Md Zabid: Acquisition and Strategic Use of Competitive Intelligence, Malaysian Journal of Library and Information Science (2011)

- Competitive Intelligence Foundation and Cipher Systems: State of the Art, Competitive Intelligence (2006)

- Hinge Research Institute: High Growth Study 2020 (2020)

- Academy of Competitive Intelligence: 2019 State of CI Impact Analysis (2019)

- Fortune Business Insights: Competitive Intelligence Tools Market, 2026 to 2034 (2026)

- Product Marketing Alliance: State of Product Marketing Report 2025 (2025)

.png)